Why the BoC Made the Move

Several factors influenced this decision:

-

The Canadian economy is showing signs of weakness: e.g., Q2 GDP contracted ~1.6%. Reuters+1

-

The labour market is softening — unemployment around 7.1% for September. Wealth Professional+1

-

Inflation remains modest and near target (~2.4% in September) though core inflation is elevated. Wealth Professional+1

-

External risks, particularly from U.S. trade policy / tariffs, are weighing on Canada’s outlook. Reuters+1

What the Rate Cut Entails

-

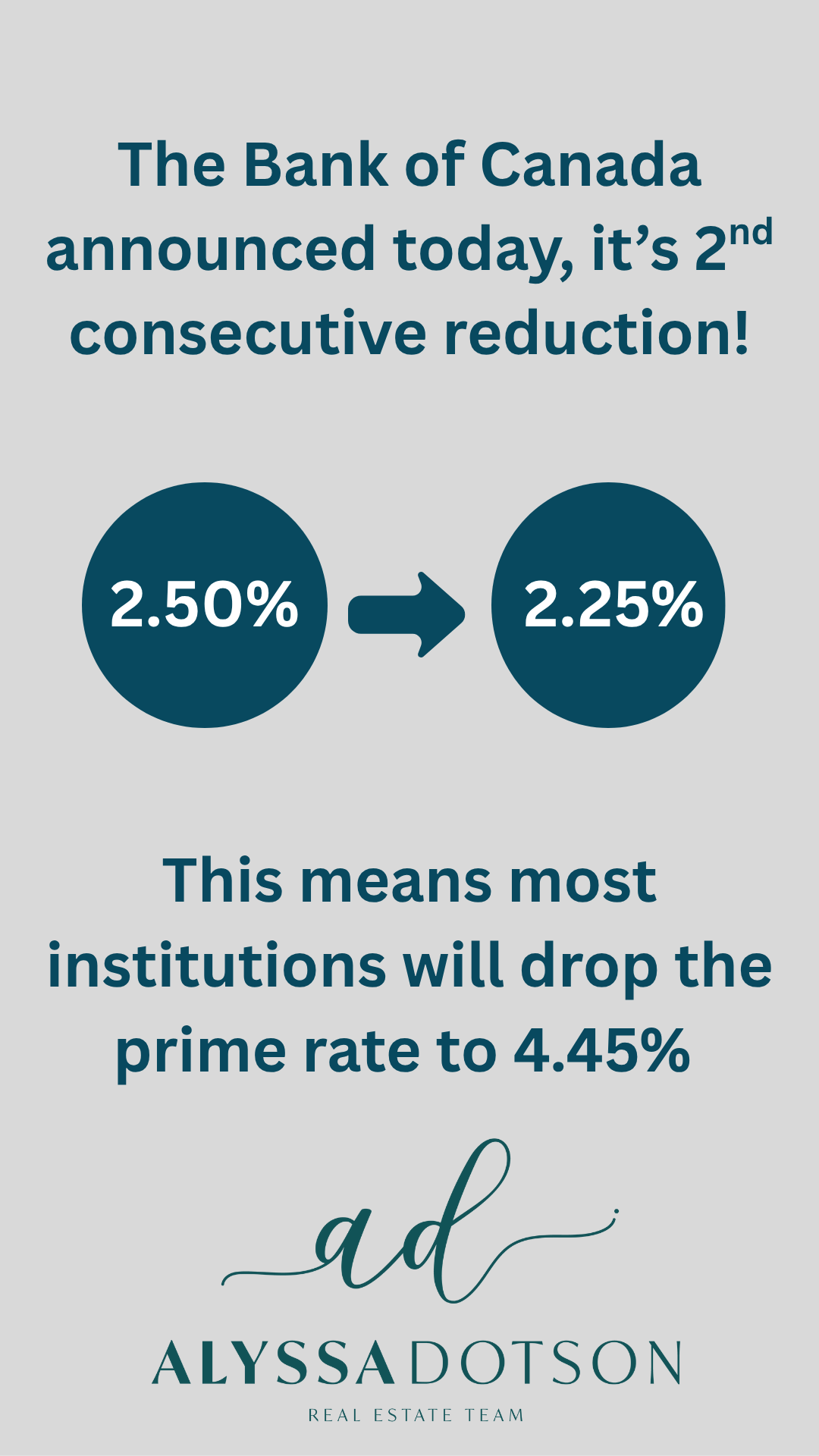

The overnight target rate is now 2.25%. Reuters+1

-

The Bank Rate and deposit rate were correspondingly adjusted (Bank Rate: 2.50%; Deposit rate: 2.20%). Reuters+1

-

The BoC indicated that while this move supports the economy, it may be the last cut for now unless risks materialize further. Reuters+1

Implications — What It Means for Consumers & Investors

For borrowers:

-

Variable-rate mortgages may become more attractive (or slightly cheaper) if banks pass along reductions.

-

Existing fixed-rate borrowers may not see a big change immediately — fixed rates are more tied to long-term bond yields.

-

Earlier commentary: “the recent rate cuts have narrowed the gap between fixed and variable-rate options.” Wealth Professional

-

For savers/investors:

-

Savings and deposit accounts may continue to see low rates; rate cuts typically reduce return in low-risk instruments.

-

Bond yields may adjust (depending on market expectation of further cuts or holds).

For real estate / housing market:

-

Some experts expect the cut to help home-buyers off the sidelines. Mortgage Professional+1

-

But with trade and growth risks, the housing market may still face headwinds (slower employment, consumer caution).

What to Watch Going Forward

-

Will inflation creep up (especially core inflation) and force the BoC into a “hold” or even tighten?

-

The evolution of the U.S.–Canada trade relationship and global economic growth.

-

Whether the BoC will cut again, and if so, how soon. Markets are uncertain: some expect no further cuts until early 2026. Reuters+1

-

How banks and lenders pass along (or don’t pass along) the rate change to consumers.

Quick Takeaways

-

Rate now 2.25% — this cut was expected and aligns with the BoC’s view of a slower growth environment.

-

Good news for variable-rate borrowers; less so for savers seeking higher returns.

-

The move doesn’t guarantee huge changes in loan or mortgage costs — timing and lender behaviour matter.

-

It signals caution: growth is fragile, inflation manageable, and external risks remain large.

-

If you’re making financial decisions (mortgage renewal, variable vs fixed rate, investment portfolio), it’s a good moment to review your options with this rate environment in mind.